PearTree Canada Founder & CEO Ron Bernbaum on how Charitable Flow-Through Financings Help Secure Exploration Capital

PearTree’s Innovation: One Financing Platform materially benefiting two very different sectors. Reducing the cost of philanthropy expands gifting while reducing the cost of resource exploration enables greater access to risk capital at reduced dilution.

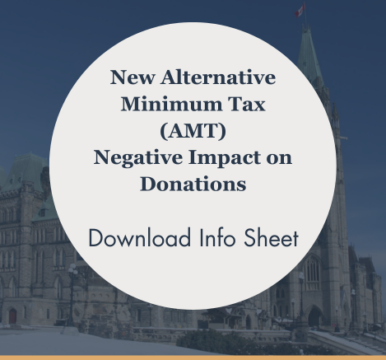

Learn More About PearTreeThis week’s federal Fall Economic Statement confirmed that the AMT changes will come into effect on January 1, 2024, but indicated that there may be room for continued public input. The exact words read “Previously Announced Measures: The 2023 Fall Economic Statement confirms the government’s intention to proceed with the following previously announced tax and related measures, as modified to take into account consultations and deliberations since their release….including …Alternative Minimum Tax for High-Income Individuals…” There is no indication as to what is being modified.

Imagine Canada Caring Companies invest a minimum of 1% of their pre-tax profits back into the communities they serve. Your company’s 1% investment can come from four main areas: cash and in-kind contributions, volunteerism, management costs, or the philanthropy side. PearTree is proud to hold The Imagine Canada Caring Company distinction.

Through our proven Flow-Through Share Donation Platform, we provide enhanced exploration capital for remote and Northern Canadian resource issuers at reduced share dilution.

Discover PearTree Mining FinanceThrough flow-through share financing, we accelerate charitable impact by accessing long-established Canadian tax incentives, decreasing the after-tax cost of giving, and facilitating transformational gifts.

Discover PearTree Philanthropy

Flow-Through Shares allow Canadian resource companies to sell shares at a premium to investors, who then donate the shares to a Canadian charity. Together, these transactions accelerate fundraising and investment efforts and reduce the investor’s taxable income.

Learn More About FTS